# Mapping trading to RL

- Environment: Market

- State:

- adjusted close/SMA (using close or SMA by itself however might not be a good choice)

- Bollinger band value

- P/E ratio

- whether we're holding stock

- return since entry

- Actions: Buy/Sell/Do Nothing

- Reward: Daily Returns (Better cause it is immediate reward), 0 until exit then cummulative return (Delayed reward)

# Markov Decision Problems

- Set of states (S)

- Set of actions (A)

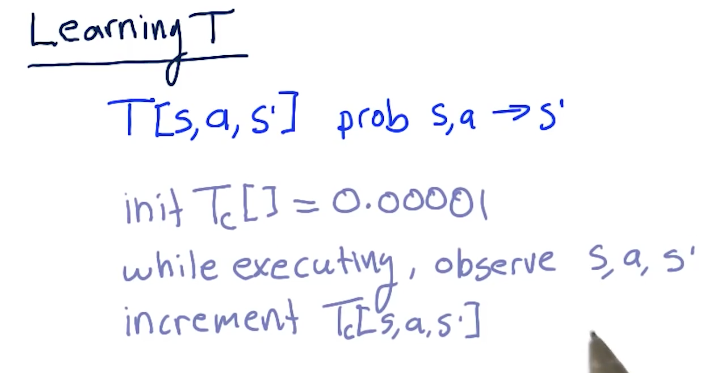

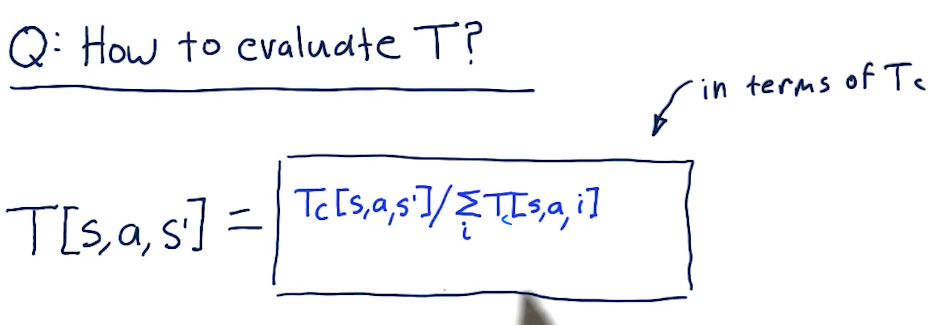

- Transition function (T) - [s, a, s']

- T is a three dimensional object and it records in each cell such that the probabibility if we are in state (s) and action (a), we will end up in state (s')

- Suppose we are in particular state (s) and take a particular action (a), the sum of all the next states we might end up in (the s's) 1.

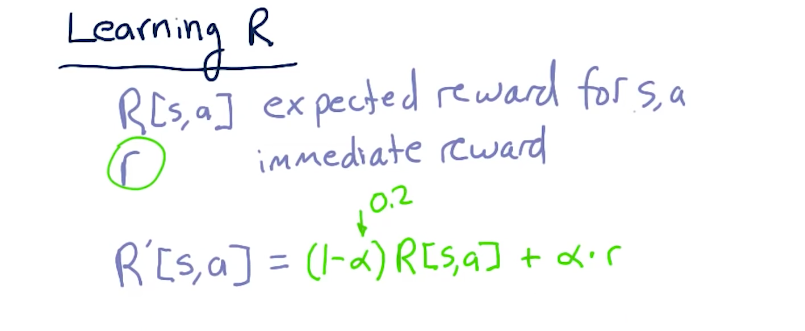

- Reward function (R) - [s, a]

- If we're in a particular state (s) and we take a particular action (a), we get a reward

- To Find: Policy (

(s)) that will maximize reward. If we get the optimal policy, we write it as (s)*

Policy iteration and Value iteration are algorithms that can be used to find the optimal policy.

For trading, since we do not have T amd R, we can't use these Policy iteration and value iteration.

# Uknown transitions and rewards

We collect experience tuples

<s1, a1, s1', r1>

<s2, a2, s2', r2>

...

The s1' is the new s2.

Once we gather a trail of experience tuples,

We can use them to compute the Policy

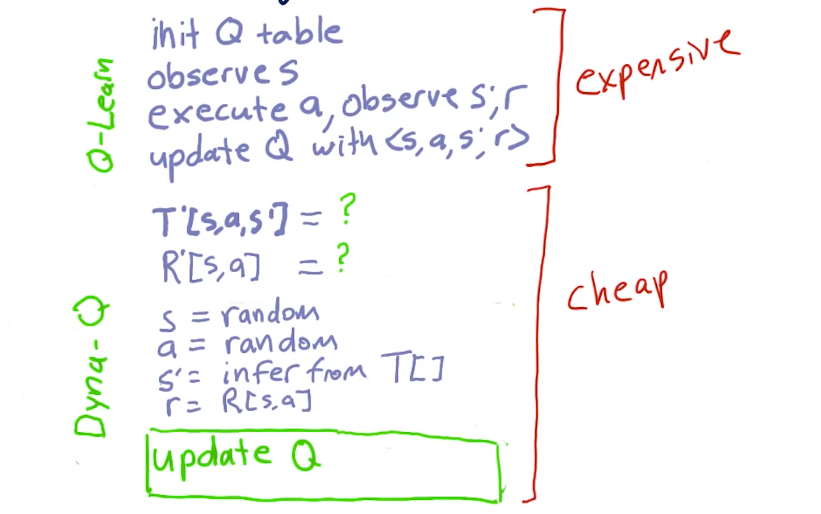

- Model based

- Build model of T

- Build model of R

- Then use value/policy iteration to find optimal policy

- Model free

- Q-learning

# What to optimize?

- Infinite horizon: You'll be collecting reward for infinite time

- Finite horizon: You'll be collecting rewaef for finite reward

- Discounted reward: Time Value of the same reward decreases over time

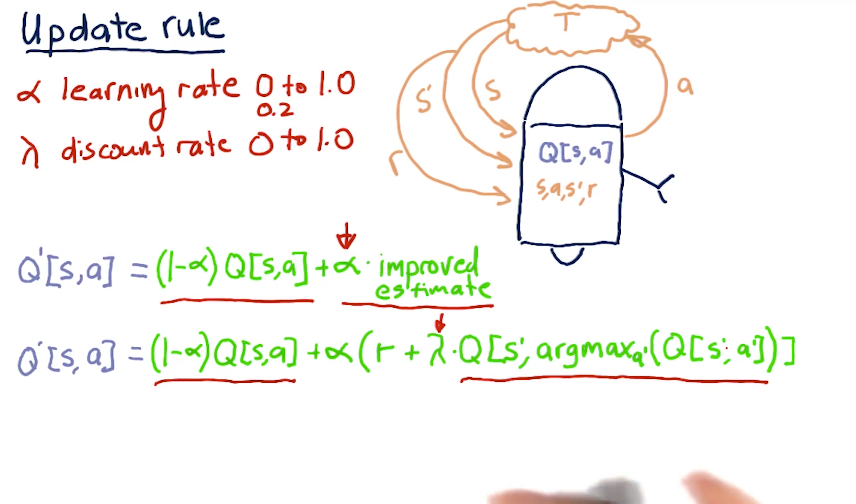

# Q-learning

First we have the Q-table

Q[s,a] = immediate reward + discounted reward

How to use Q?

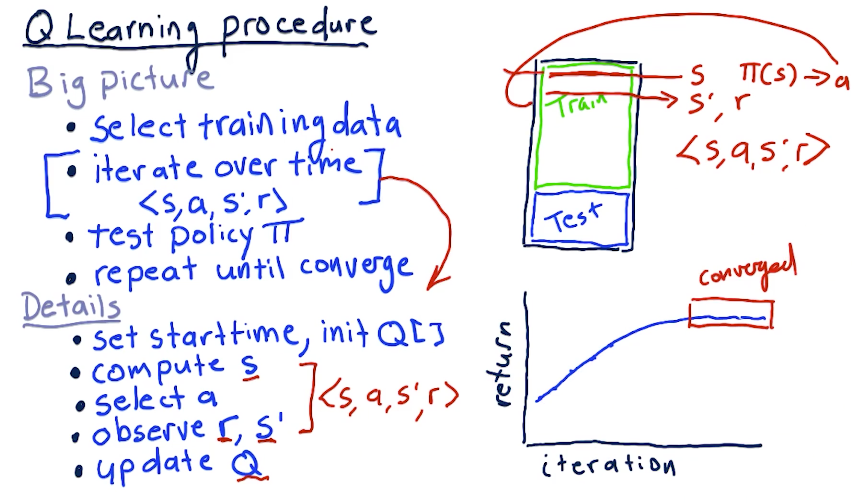

# Learning Procedure

# Update Rule

# Finer Points

- Success depends on exploration

- Choose random action with probability c

- Coin Flip 1: Are we going to pick random action or action with best Q value?

- Coin Flip 2: Which of the random actions are we going to select?

- Picking 0.3 is considered a good value for c

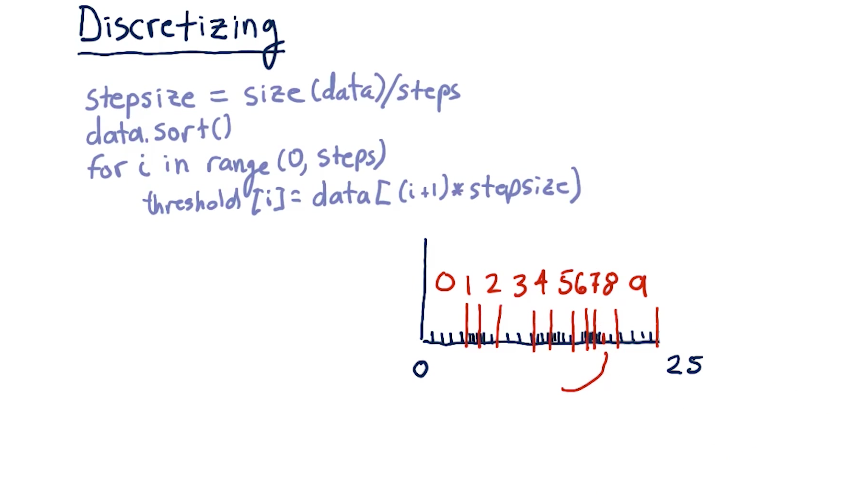

# Creating the state

- state is an integer

- discretize each factor

- combine each of multiple factors to one integer

- If the four factors return 0, 4, 2, 6, the single integer for state becomes 0426

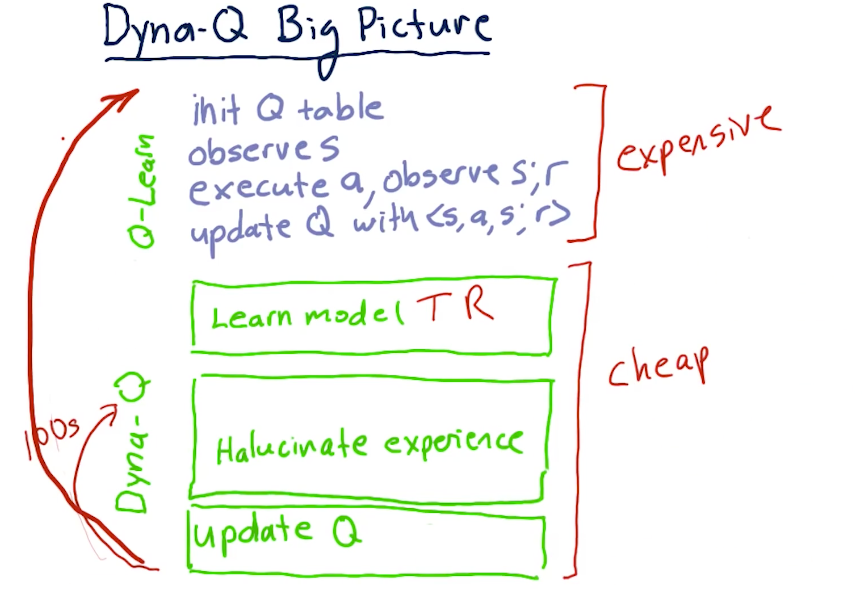

# Dyna

Blend of Model-based and Model-free learning.

Since Qlearning does not use T and R, Dyna allows Qlearning to do that.